A new LP Proficiency Survey has been released disclosing the most comprehensive study into the sophistication of private equity’s fund investors. This research has been carried out by eFront, a financial software and solutions provider dedicated to Alternative Investments.

The report, which canvassed the opinions of LPs ranging from high net worth individuals to major pension plans, finds that investors are falling short of industry best practice in areas such as negotiation, reporting and position monitoring. In all, 179 investors from across the globe rated their approach to 10 private equity investment competencies, selecting from answers graded in terms of sophistication.

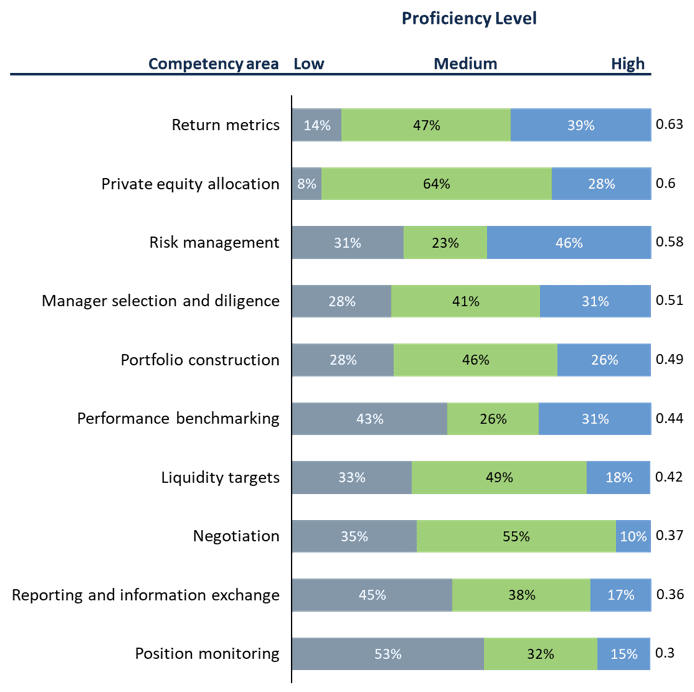

Key findings:

The weakest categories for LPs were:

- Negotiation, where more than a third of LPs (35%) do not attempt to seek better alignment with GPs or separate accounts

- Reporting, where nearly half (45%) of investors rely entirely on GP-provided material and do not seek standardized / digitized information that supports advanced analytics

- Position monitoring, where more than half of investors (53%) use the simplest form of monitoring, failing to leverage integrated systems for analytics and industry-wide transaction libraries

The strongest metrics for LPs were:

- Private equity allocation, where more than 90% of respondents display a high or medium level of proficiency

- Return metrics, where more than 85% of investors use sophisticated methods to measure performance

- Risk management, where 46% take a rounded and comprehensive approach – though at the same time nearly a third (31%) use the very simplest, least comprehensive measures. (Given that this is the competency area with largest dispersion in answers, the benchmarks are less clearly defined.)

Tarek Chouman, CEO of eFront, commented: “There is no shortage of commentary about the value created by general partners of private equity funds. Much less consideration is given to the value added by the proficient and engaged limited partner. And yet such is the complexity of managing a portfolio of private equity funds, and such is the range of sophistication in how LPs approach this challenge, that the LP value creation dynamic ought to be a major consideration.”

eFront’s analysis showed that, while investors perform very well across a number of key metrics, their sophistication score sits below half marks in six of the ten skill categories studied. LPs performed particularly poorly in negotiation, where more than a third focus on very simple negotiating points. Meanwhile, just a tenth seek a segregated account or the option to make the final decision on capital deployment.

In reporting and information exchange, there is significant variation in sophistication. The largest proportion of LPs (45%) passively accept GP information and do no detailed analysis of NAV or distributions, while only 17% of the respondents in the survey reported that they employ the use of platforms that collect and streamline this type of report.

LPs received their lowest score in position monitoring, where more than half of investors (53%) use the simplest form of monitoring and just 15% exploit integrated systems that pair proprietary data with third-party sources, enabling sophisticated analysis.

On the positive side, LPs appear to be highly proficient at determining the appropriate private market allocation. This competency has the least divergence among the investors, and the fewest low scores, with just 8% of investors passively following their peer group to determine allocations. Indeed, no pension fund or fund of funds respondents followed this least sophisticated strategy.

Performance measurement, meanwhile, is the area of greatest proficiency among LPs, with more than 85% of investors using sophisticated methods and just 14% of respondents using a simple IRR calculation to measure performance.

Risk measurement was the third-strongest category, but the way LPs measure risk varies greatly. This may indicate that there are no clearly established benchmarks in this competency area and that self-assessment choice depends on the internally defined benchmarks within each organization. Almost a third of respondents devise a simple metric which is equivalent to public market volatility; almost a quarter use Value-at-Risk methodology and track correlations between values of different positions in portfolio; and 46% take a comprehensive and rounded approach, encompassing specific metrics and extraneous risks.

Tarek Chouman commented: “You might think that respondents would be tempted to inflate their own sophistication, and it is possible that there is some confidence bias in the results. But the overall picture is endlessly revealing. The highest area of proficiency is in return measurement, while areas of relatively poor proficiency, such as liquidity targets, negotiating priorities, position management, benchmarking and information exchange leave the most room for improvement in performance. Equally fascinating is how different investor types vary in sophistication. While there is inevitably an advantage for larger players, this is by no means the case across all competencies.”

HedgeThink.com is the fund industry’s leading news, research and analysis source for individual and institutional accredited investors and professionals

{kind=link}