Institutional investment management is broken. Asset gathering business objectives and gold-plated cost structures magnify the imperative to grow AuM. Investment firms led by marketers rather than investment managers create strategies tailored to what will sell rather than what works. Large pools of management fees are required to fund large, expensive, teams designed to convey analytical edge. Pressures to justify high management fees discourage investment professionals from acknowledging ignorance or mistakes and create an action bias that is antithetical to good investment outcomes.

By Mark Walker, Managing Partner at Tollymore Investment Partners

The creation and promotion of investment strategies that will sell result in niche investment universes predicated on analytical edge, primary research methods, or proprietary idea generation funnels, all of which look ‘differentiated’ in a pitchbook. The latest incarnation of this pitchbook mentality comes in the form of ESG investing mandates.

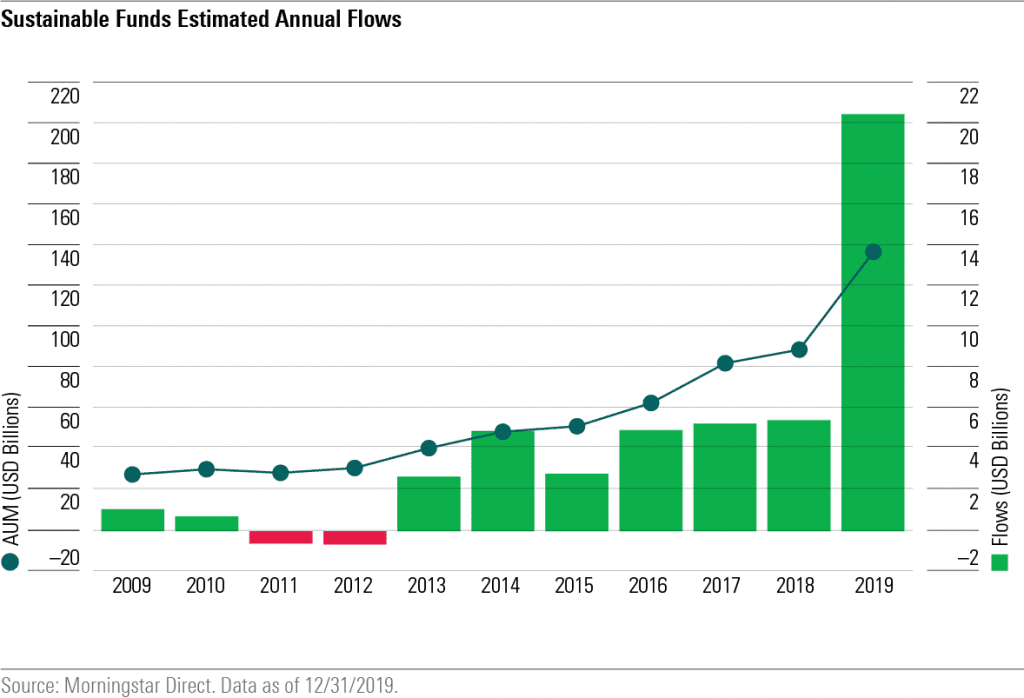

Investors last year ploughed a record $21bn into ‘socially-responsible’ investment funds in the US, almost quadrupling the rate of inflows in 2018. The surge in popularity of companies with the best social, environmental and social governance scores in recent times has resulted in a crop of ESG funds, eager to attract some of the cyclical capital flows to this bucket.

Attempts to quantify art through an obsession with measurement creates bubbles, disincentivises first principles thinking, and makes capital allocation and manager selection processes less efficient by making them more data driven. But data can be falsely empowering, unaccompanied by thoughtful qualitative review of a manager’s capacity and incentives to do a good job.

The shoehorning of ESG frameworks into existing asset management programmes and the surge in new ESG funds extend the already warped incentives in the investment management industry. Stocks with strong ESG scores are bid up as these capital inflows are put to work. Are investment managers, guided by the desire to grow assets and the employment of a quantitative ESG scoring framework, and absent the facility to think independently about the sustainability and reasonable governance of companies, and the investment merits of their equity, being socially responsible by directing endowments’, charities’ and pension funds’ capital to this more richly valued subset of the global investment universe?

ESG’s commonly accepted synonymity with ‘sustainable investing’ is especially perplexing. Who wants to own unsustainable businesses? What is investing if not the purchase of part-ownership of sustainable, flourishing enterprises? What long term business owner, managing capital for investors with long term, sometimes perpetual, investment horizons, would like the company she owns to be run by dishonest, self-serving managers misaligned with company owners, to treat employees poorly, create negative externalities, and exploit its customers? The studious long-term investor must consider the company’s relationship with all its stakeholders. At a minimum, understanding the strength of these relationships is central to mitigating risk of permanent capital erosion. Ideally, these relationships confer a lasting unfair business advantage, difficult to replicate by peers merely paying lip service to regulators and investors requiring the completion of ESG checklists. The items on these checklists must be measurable. This encourages the quantification of factors which are qualitative. How can one quantify, or score, whether, and the extent to which, social media companies exploit their users to the detriment of their health? Can these checklists consider and measure the enormous and compounding positive externalities created by modern platform businesses? An appreciation of the relationship between a company and its stakeholders is a qualitative, subtle, and effortful endeavour. The interrogation of business ethics and the capacity for company managers to make the right long-term decisions are at the heart of serious investment programmes. The employment of an outside analytics firm to bestow credibility on an ESG framework is no part of this.

Any investor with an interest in owning sustainable businesses must recognise that company boards have broader responsibilities to consider environmental and social issues. They will also understand that these duties do not dilute their fiduciary obligations to equity holders. Rather, they are a necessary part of satisfying them. Decisions to create large positive externalities and forge win-win outcomes – non-zero-sumness – take time and often come at the expense of traditional short-term measures of shareholder return. But these are the decisions that determine corporate vitality and staying power.

The broad disregard for long term win-win outcomes is a function of short holding periods. Company ownership changes hands on average every few months, vs. eight years in the 1960s. This is a by-product of investment constraints deeply embedded in the institutional money management industry, such as short-term capital, manager/investor misalignment, career risk and asset-growth agendas. These constraints cannot be addressed with an ESG checklist.

“The surge in popularity of companies with the best social, environmental and social governance scores in recent times has resulted in a crop of ESG funds.”

Just as truly special corporations seek to thrive under the principle of win-win, so must investment management firms create more value than they consume. Incentive structures should make it sensible to forgo additional management fees in lieu of excess returns on insider capital. Frameworks for economic profit-sharing should reward acceptable performance and coordinate manager and investor enrichment. Investors should receive most of any outperformance generated, not just most of the absolute return. Fee structures should therefore allow fund managers to talk about integrity with some legitimacy. Too many managers charge egregious fees with the sole purpose of enriching themselves at the expense of clients.

With business ownership in the public markets so fleeting, and given the strong economic incentive to raise capital, it is unsurprising that the objective of investing in viable, durable companies is not evergreen nor widely practised. This is a sombre impeachment of the asset management industry. But it creates opportunity for those investors who recognise that treating stakeholders well is good for business owners. We look for symbiotic value chains; there need not be a trade-off between compounding owners’ capital and the principled consideration of all other lives our companies affect. Managers of the companies we own must look beyond the direct or immediate consequences of their actions in order to create lasting value. And a long-term outlook is essential, because shorter term sacrifices – ‘the capacity to suffer’ – are often required to create value of any permanence.

HedgeThink.com is the fund industry’s leading news, research and analysis source for individual and institutional accredited investors and professionals

{kind=link}