Creators of first cryptocurrencies had the intention to create a new means of payment for use by the general public. However, the early day coins have not evolved into a new means of payment or store of value, but have served more as a highly speculative asset class for certain investors. Also, several kinds of research suggested that those who do use coins like Bitcoin as a means of payment, primarily do so for illegal purposes on illegal markets.

To understand what stablecoins are all about, let’s see how they differ from popular cryptocurrencies like Bitcoin, Litecoin or Bitcoin Cash.

The main reason the first wave of cryptocurrencies are not used as a means of payment is because of the highly volatile price. They are not backed by any underlying asset, claim or liability, and this makes them prone to serious fluctuations.

Coins that fail to hold a steady value generally fail to have the indicia of money: function both as a medium of exchange, a unit of account and a store of value.

What are Stablecoins?

For now, the term “stablecoin” does not have an agreed definition. At the most basic level, stablecoins are a new type of cryptocurrencies that are backed by something of value. There are various definitions of stablecoins from legal scholars and institutions, such as:

- digital units of value that are not a form of any specific currency but rely on a set of stabilisation tools which are supposed to minimise their volatility;

- a new class of cryptocurrencies which offer price stability and/or are backed by reserve assets, combining the instant processing and security of payments of cryptocurrencies, and the volatility-free stable valuations of fiat currencies;

- coins that represent a claim, either on a specific issuer or on underlying assets or funds, or some other right or interest; and

- cryptocurrencies designed to maintain a stable market value relative to another asset (typically a unit of currency).

Unlike most traditional “non-backed” cryptocurrencies, stablecoins typically have an identifiable issuer. Such third-party accountable institutions (e.g., custodians) can be held responsible by regulators and users.

Like traditional “non-backed” cryptocurrencies, stablecoins are crypto-assets. They are private and digital in nature and they use distributed ledger, often an existing blockchain.

Many stablecoins have already been in circulation for several years. The first stablecoin, Tether (USDT) dates back from 2014 and other stablecoin projects like Gemini Dollar (GUSD) and Paxos Standard (PAX) are nearing their second birthday.

Stablecoin Types

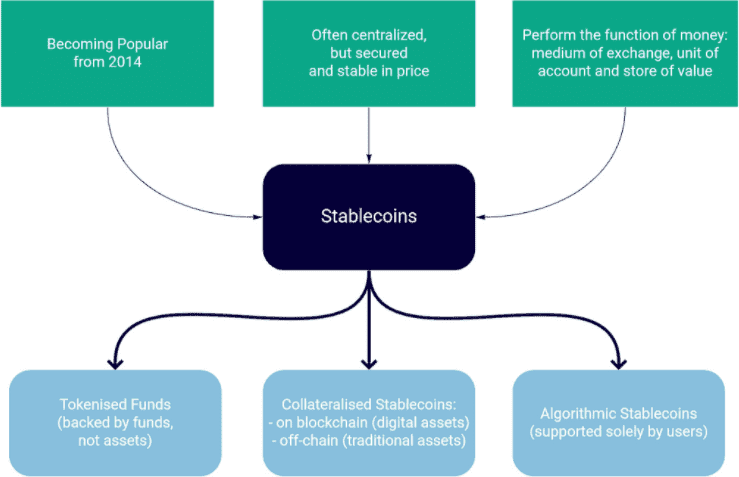

As their name suggests, stablecoins make use of so-called “stabilisation mechanisms”. Their value is backed by “something” allowing them to maintain a stable value. This Something determines three broad categories, as visually illustrated in Figure 3:

Stablecoin features (top) and types (bottom).

The first category of stablecoins is supported by funds, sometimes also referred to as “tokenised funds”. It relates to units of monetary value that are stored electronically in a distributed ledger to represent a claim on an issuer. The issuer holds the funds or involves a custodian for that purpose, and ensures that the funds backing the stablecoins are redeemable (at par value).

The second category of stablecoins that can be distinguished, is the category that is supported by assets other than funds against which users can redeem their holdings. The coins that fall within this category are referred to as a “collateralised stablecoins” and, broadly speaking, come in two variants:

- The first variant is supported by traditional assets, such as commodities and real estate, and typically requires a custodian for safekeeping. The coins that fall within this category are called “off-chain collateralised stablecoins”;

- The second variant is supported by assets in digital form, typically other crypto-assets. They can be held in a decentralised manner. The coins that fall within this category (like Multi-collateral DAI) are called “on-chain collateralised stablecoins”.

Coins can also be stabilised with collateral by linking their value to a basket of reference assets. Such basket can include commodities and real estate, but also government securities and fiat currencies. The stabilisation mechanism usually works much like an exchange-traded fund, where the holder does not own the underlying assets.

The third category is a bit unusual, as it is supported solely by users’ expectations about the future purchasing power of their holdings. Such coins are often referred to as “algorithmic stablecoins”. They seek to maintain par value with a currency of reference through algorithmic trading, i.e. by automatically adjusting the supply of stablecoin units. Algorithmic stablecoins do not require the accountability of any party, nor the custody of any underlying asset. With the exception of NuBits, which failed to deliver on the promise of stability, most initiatives are still in the development phase.

Most stablecoin initiatives currently on the market are for retail purposes (can be used by anyone). An example of a wholesale stablecoin (for a select number of actors) is JPM Coin.

Global and Local Stablecoins

However stablecoins can be traded on crypto-exchanges on a 24/7 basis, from nearly anywhere in the world, their actual footprint usually remains local.

Recently, new stablecoin initiatives have emerged. The most important one is probably Facebook’s Libra project. These new initiatives that are built on top of existing, large and/or cross-border user bases. They can also be monitored fairly easily using a cryptocurrency transaction monitoring service, and have the potential to scale very quickly to achieve a global or other substantial footprint and are commonly referred to as “global stablecoins”. Global stablecoins are currently under a lot of scrutiny, because they could pose significant risks to financial stability and monetary policy.

This is an article provided by our partners’ network. It does not reflect the views or opinions of our editorial team and management.

Read More:

what is one benefit to working collaboratively on a team?

how would you reconcile your bank account to avoid spending more than you have?

how is having a security system for your home a risk management strategy?

Peyman Khosravani is a global blockchain and digital transformation expert with a passion for marketing, futuristic ideas, analytics insights, startup businesses, and effective communications. He has extensive experience in blockchain and DeFi projects and is committed to using technology to bring justice and fairness to society and promote freedom. Peyman has worked with international organizations to improve digital transformation strategies and data-gathering strategies that help identify customer touchpoints and sources of data that tell the story of what is happening. With his expertise in blockchain, digital transformation, marketing, analytics insights, startup businesses, and effective communications, Peyman is dedicated to helping businesses succeed in the digital age. He believes that technology can be used as a tool for positive change in the world.