Financial education has become an important complement to market conduct and prudential regulation and many countries have made improving individual financial behaviours a long-term policy priority. These words, said by the OECD, reflects a growing concern worldwide: innovation in finance is moving faster than consumers and many financial services. And the only way to keep up with it is by investing in education. In a world dominated by continuum technological advances, the efforts towards financial education shouldn’t be limited to economic affairs but rather focus on mastering the technology that will drive the financial mechanisms of the future.

The statement “Finance rules the world, but soon technology will rule finance” is as real as it has ever been. Recent innovations brought by technology have changed the way consumers approach new services, modifying their behaviour along the way. E-commerce, social media and streaming platforms are only a few examples where consumers have changed their habits toward technology-powered solutions. In the finance space -traditionally reluctant to fast paced innovations-, fintechs are taking the industry by storm, and the revolution is on its way.

The Financial Stability Board divided fintech into five broad categories: payments, clearing and settlement; deposit, lending and capital raising; insurance; investment management; and market support. The success of Fintech startups like Revolut, Alipay, Ant Financial or SoFi have made traditional financial institutions adopt their innovations into their own systems at a pace that these massive and complex companies can’t barely keep up with. 70% of global CEOs are concerned about the speed change in technology in the financial sector. This points to a growing issue: There’s a shortage of talent with the right skills to integrate new technology into existing systems within industries disrupted by technology. This is a big issue in finance already and will only become a greater problem as fintech’s presence increases.

A Shortage of Talent

The advances that Fintechs promise are possible through data and efficiency and require data analytics and other technology-related roles. “Platforms use alternative data sources, such as utility bills and predictive information, to understand their customers financial lives and assess their ability to repay. Relying on this data, they can create products tailored to their customers, for example providing loans based on cash flow instead of collateral. This enables borrowers without significant wealth or assets such as a home or land to get a loan. And as operational efficiencies increase with improved technology, costs decrease and Fintech platforms can afford to serve harder to reach customers who need small loans – something that traditional banks won’t do,” summarized Forbes’ expert Jennifer Pryce in a recent article. The key aspect in Fintech is maximizing technology to come up with innovative solutions. In other words, Fintechs make finance fast and easy to understand for the majority of consumers while providing tailored solutions. Here, the underlying problem is on the other side of the spectrum, banks and fintechs need technologists, not bankers.

A recent research by workplace accreditation body Investors in People found that 66% of vacancies in FinTech jobs and also in the InsurTech sector need candidates to have certain digital skills. In fact, skills and access to talent represent a major hurdle. According to the Open University, 75% of FinTech firms fear a skills crisis over the next 3 years and 44% of them claim that finding the right talent represents a vital challenge for their business. Crucially, the European Commission predicts that the UK will have a shortage of 249,000 workers for technologically skilled jobs this year.

Likewise, data from the World Economic Forum says that “the talent deficit is driven both by rapid growth of the fintech sector and by a major shift in the types of roles in financial services more broadly.” Emerging roles – including data analysts, AI and machine learning specialists, designers, people who work in innovation roles – who currently account for 15% of the financial services workforce, are expected to account for 29% of the workforce by 2022.

To address this global talent shortage within finance, we need to start building the necessary skills at a young age. This will grow the next generation of financial professionals who are well versed in technology and its potential and who will help propel the industry into the future. To prepare for the future of finance, governments and businesses should invest in domestic talent by partnering with educational institutions to develop fintech skills. Incorporating the right education is key to ready students for the financial world they’ll eventually enter.

Global programs are beginning to adapt for this need, with Asia being a region to watch. Experts predict that Asia will emerge as “a key center of technology-driven innovation” in the financial sector. As a leader in innovation and schooling, we can look to Singapore to see how a country and institutions within it can promote readying students for the future of finance.

Especially significant is Singapore. The city-state is a prime example of government and institutional support for creating programs that ready the workforce to tackle the impending revolution. It’s working on becoming the top fintech hub in the world and betting on education programs to get there. The Monetary Authority of Singapore (MAS) has committed to invest S$225 million (around US$167 million) to provide support to reach this goal over a five year period.

At the college level, curriculums are introducing fintech as a subject in itself, incorporating expertise from businesses to inform the programs. One leading university in Singapore is collaborating with a top technology company to develop a fintech curriculum. Other schools are following suit globally, with business schools in places like New York and Europe now offering classes or majors in the subject. Fintech summits are also a big incubator for enhancing education in the field.

Ultimately, investing in youth is imperative for a country’s success. And countries and businesses should look to Singapore for inspiration, as it sits at the top of the human capital index—a measure of youth lifespan, schooling, and health. With the rise of technology, it’s smart for education to adapt accordingly to prepare their students for the future.

A long road ahead

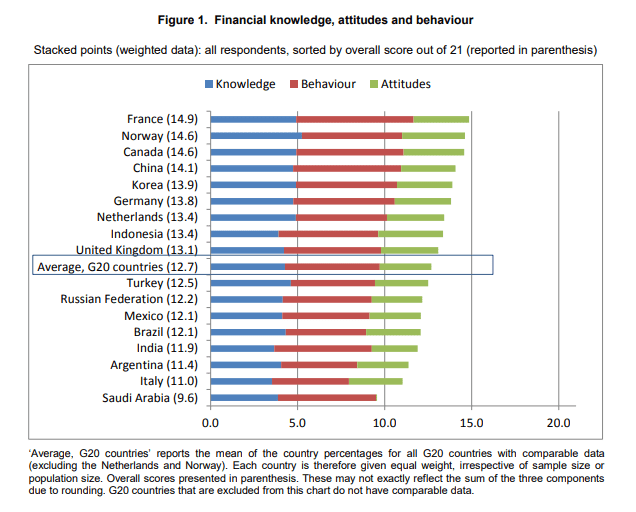

However, countries aren’t advancing as fast as it seems they should. Around one in four students in the 20 countries and economies that took part in the latest OECD Programme for International Student Assessment (PISA) test of financial literacy, and one in seven in the 13 OECD countries and economies, are unable to make even simple decisions on everyday spending.

The PISA report also showed that only one in ten students performs at the highest level of financial literacy, on average across OECD countries and economies; these students are able to make financial decisions in contexts that will only become relevant to them later in life.

Estonia had the highest average score, followed by Finland, the participating Canadian provinces (British Columbia, Manitoba, New Brunswick, Newfoundland and Labrador, Nova Scotia, Ontario and Prince Edward Island), Poland and Australia.

Some 117,000 15‑year-olds took part in the test, which evaluated the knowledge and skills of teenagers as regards money matters and personal finance. Items in the assessment addressed topics such as dealing with bank accounts and debit cards, understanding interest rates on a loan, or choosing between a variety of mobile phone plans. This is the third time that PISA has assessed students’ ability to face real-life situations involving financial issues and decisions.

Simon Pearson is an independent financial innovation, fintech, asset management, investment trading researcher and writer in the website blog simonpearson.net.

Simon Pearson is finishing his new book Financial Innovation 360. In this upcoming book, he describes the 360 impact of financial innovation and Fintech in the financial world. The book researches how the 4IR digital transformation revolution is changing the financial industry with mobile APP new payment solutions, AI chatbots and data learning, open APIs, blockchain digital assets new possibilities and 5G technologies among others. These technologies are changing the face of finance, trading and investment industries in building a new financial digital ID driven world of value.

Simon Pearson believes that as a result of the emerging innovation we will have increasing disruption and different velocities in financial services. Financial clubs and communities will lead the new emergent financial markets. The upcoming emergence of a financial ecosystem interlinked and divided at the same time by geopolitics will create increasing digital-driven value, new emerging community fintech club banks, stock exchanges creating elite ecosystems, trading houses having to become schools of investment and trading. Simon Pearson believes particular in continuous learning, education and close digital and offline clubs driving the world financial ecosystem and economy divided in increasing digital velocities and geopolitics/populism as at the same time the world population gets older and countries, central banks face the biggest challenge with the present and future of money and finance.

Simon Pearson has studied financial markets for over 20 years and is particularly interested in how to use research, education and digital innovation tools to increase value creation and preservation of wealth and at the same time create value. He trades and invests and loves to learn and look at trends and best ways to innovate in financial markets 360.

Simon Pearson is a prolific writer of articles and research for a variety of organisations including the hedgethink.com. He has a Medium profile, is on twitter https://twitter.com/simonpearson

Simon Pearson writing generally takes two forms – opinion pieces and research papers. His first book Financial Innovation 360 will come in 2020.