Value Proposition of Hedge Funds

In order to succeed in the modern world of finance, adaptability is the key. The same is the case with active investment management, which is completely reliant on change and its ability to capitalize on it.

Active risk management only works well if the skills and abilities of individuals are applied in such a way that they earn rewards in the market, and the chances of risk or reward are greater for the individual who is taking the risk. Still, this is not a sure way of using ones skills to earn rewards. There are numerous instances where successful ideas and techniques are plagiarized and the market becomes unresponsive to the skills that are being applied, which essentially mean that the markets become more effective and efficient. Thus, the skills that are applied in the market should be able to adapt to changes easily and continue evolving in order to maintain their value and importance in the market.

Passive vs. Active Risk Management

It is important to keep in mind the difference in the definition of risk that is taken in the case of relative return, as opposed to absolute return, to fully understand the benefit of hedge funds. Whatever the name of hedge funds might suggest, they do take risks. This means that all risks are not hedged. However, risk can be controlled in some instances, which means that some risk is taken intentionally while other risks can be hedged.

The concept of a modern hedge fund is that it acts as an active risk manager, thus proving that the risk that investors get is not from a market. If we keep this definition in mind, two reasons can be attributed to a manager who keeps a market benchmark as being a passive manager.

The first reason is that the way the funds of a manager perform depends largely on the market benchmark. The revenue that is being earned in this case can be achieved more cheaply than paying an active fee for it. The second reason is that the manager is not obliged to reduce the expense of capital depreciation.

These two reasons clearly show the difference between a long-only fund and hedge fund, which is that the risk of the former is determined by the market, while the latters risk is reliant on the judgment of the hedge manager.

Hedge Fund and Active Risk Management are Interchangeable

The word active is generally used to describe a manager who is long-only and has the authority to increase or decrease the number of securities compared with a set benchmark. Analyzing this terminology gives us the ability to distinguish between an index fund and a mutual fund, where the former has no freedom. On the other hand, the term passive is used when talking about an index-fund. However, it becomes hard to differentiate a long-only manager of an index fund in an equity bear market. In both cases, the investors can lose up to 50 percent of the amount of capital invested. On the other hand, it is not necessary for a hedge fund to suffer loss when the market falls. The manager of the hedge fund may have been able to hedge all equity exposures since they have the authority and discretion over the entire portfolio. Long-only portfolio and index funds have similar risk features when the market is in distress. Hedge funds, on the other hand, might not or might have been exposed to the market in times of stress. Therefore, it is better to use the term active and passive investment management when talking about hedge funds.

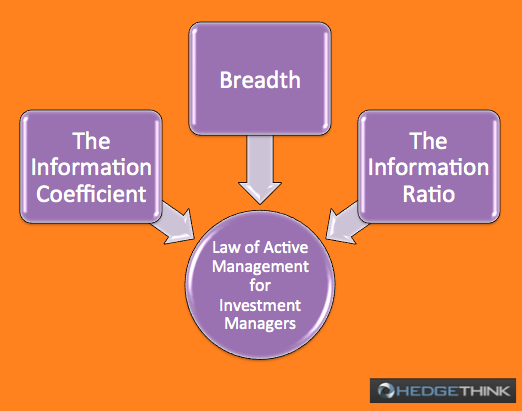

The Fundamental Law of Active Management

The fundamental law of active management is the foundation and reasoning for allowing investment managers a greater degree of flexibility in the area of their expertise. This law essentially has three features, which are as follows.

- The Information Coefficient: This is the correlation between the actual events subsequently realized and the future forecasts of returns. This ratio, therefore, helps to measure the skill.

- Breadth.

- The Information Ratio: This ratio measures the number of opportunities and chances that a successful investment manager has had to apply and take advantage of with his or her skills

Related Posts:

Roadmap to Hedge Funds – Part 1 : What exactly is a Hedge Fund?

HedgeThink.com is the fund industry’s leading news, research and analysis source for individual and institutional accredited investors and professionals