A UK business could be eligible for a Coronavirus Business Interruption Loan Scheme (CBILS), as set out by the UK Government. However, it appears that despite the Government’s best intentions, this scheme is not working in practice and some urgent readdress is required. There is, therefore, a serious concern that small businesses will start to fail in droves within weeks unless urgent corrective action is implemented.

What does the CBILS offer?

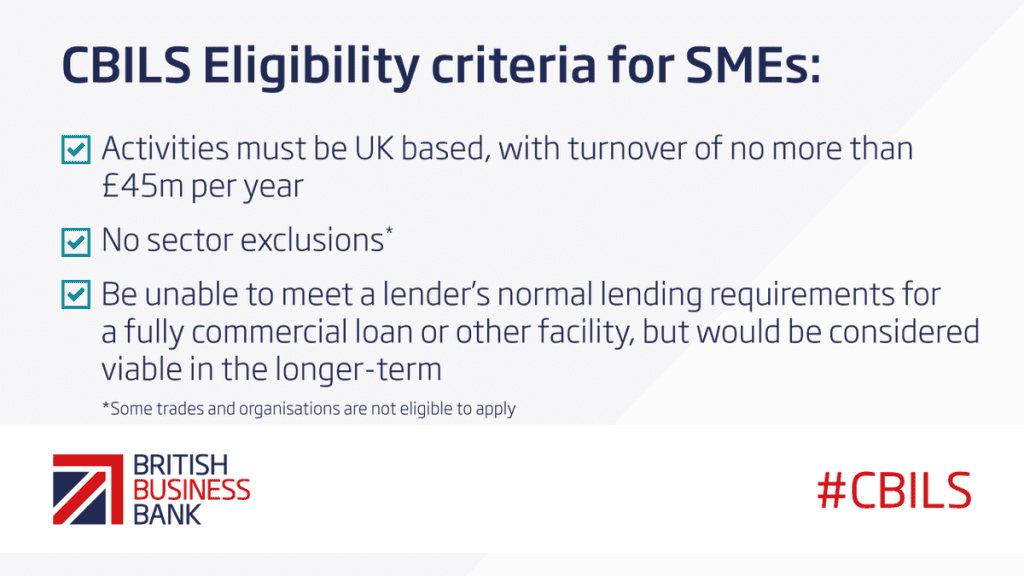

This scheme is designed to support UK based small and medium-sized enterprises (SMEs), with a turnover of up to £45 million, with a viable business proposition but are struggling with the challenges of the COVID-19 outbreak. Some key highlight of the CBILS:

· The term is 1 to 6 years;

· The loan is interest free for the first 12 months. After 12 months, interest will be charged at a variable rate or an applicable fixed rate;

· There are no set up fees;

· A capital repayment holiday is available for up to 6 months (where appropriate); and

· Loans are available from over £25k to £5m subject to affordability and criteria.

What criteria need to be met by businesses & what are the risks?

The Government under the scheme states the maximum loan amount for any business is 25% of the 2019 annual turnover or double the annual wage bill, whichever is the greater. The hurdles that businesses will have to jump over and therefore what the banks will need include:

· Confirmation of the annual wage bill in 2019 and the number of employees;

· Evidence of how the requested funding amount has been arrived at and what costs it is to cover (i.e. how will the funds be used to address the cash shortfall caused by COVID-19?);

· Details pertaining to what the business has done to streamline costs and what action has been/ is being taken in respect of other options such as Government grants & support, deferring payments, staff numbers/ costs, etc.;

· Assessment of affordability as any loan will need to be paid back; and

· Trading/ financial performance through the calendar year 2019 will be an important part of the affordability assessment as will historic performance in 2018 and 2017 etc.

This last point unfortunately might mean that loss making businesses that are viable going concerns may still not qualify.

How are commercial banks implementing this scheme?

There is unfortunately no consistency in the approach of commercial banks in the UK.

Some banks only publish loan rates under the scheme for loans up to £25,000 and one particular bank recently quoted to SME businesses a rate of 8.9% (its normal unsecured loan scheme to businesses for this level of lending is 9.9% representative APR), whilst others have been quoting rates as high as 30%. This is obscenely high especially given the recent reduction in the Bank of England base rate from 0.75% to 0.25% in an emergency response to the “economic shock” of the coronavirus outbreak.

Some risk experts have cited that the rate of interest for an 80% Government backed loan should be priced at between 1-3%.

Further, shockingly, one particular bank requested security as follows in respect of any request for funding under the CBILS namely:

“SECURITY – THE FOLLOWING SECURITY WILL BE REQUIRED BY THE BANK TO SECURE THE LOAN:

· Loan amount £25k to £100k – Unsecured (other than the Government guarantee as part of the CBILS)

· £100,001 to £250k – Debenture

· £250,001 to £1m – Personal Guarantee, Debenture and we will need to exhaust all other Tangible Security (normally property).”

This means that some banks are demanding at least £100,000 in collateral as Debenture (a long-term security yielding a fixed rate of interest, issued by a company and secured against assets). Businesses wanting to borrow more than £250,000 are being asked by banks that their directors must provide personal guarantees. That means that if the loan goes bad owing to the crisis, their personal property is at risk. The small print from one bank cites the following: “In the event of your default, we will follow our standard commercial recovery procedures, including the realisation of security, personal guarantees, if applicable, before we make a claim on the Government guarantee.”

Are SMEs being dealt a bad hand & what is the economic impact?

The banks were bailed out by the Government post 2008 and they were all too happy to accept that. There is an ethical and moral responsibility as a bank, which at a time of crises should shine through. Sadly many are seeing this as a time to profit from other’s pain and increase the bottom line when millions of individuals and thousands of businesses are struggling to survive. Research from a network of accountants cited by the BBC suggested between 800,000 to 1 million businesses nationwide could be forced to close because they can no longer cover expenses. It is predicted that nearly a fifth of all small and medium-sized businesses in the UK are unlikely to get the cash they need to survive the next four weeks, in spite of unprecedented Government support.

SMEs are the backbone of the UK economy and to understand the impact this may have, which could be catastrophic for UK GDP and jobs, one only has to look at the statistics:

· According to the Federation of Small Businesses (‘FSB’), in 2018, SMEs accounted for 99.9% of the business population (5.9 million businesses).

· SMEs accounted for three fifths of the employment and around half of turnover in the UK private sector.

· Total employment in SMEs was 16.6 million (60% of the total), whilst the turnover was estimated at £2.2 trillion (52%). While still small in the overall UK market.

· SME lending was increasingly an underserved sector before this and the current crises only serve to highlight that there are fundamental structural changes needed in this going forward. But first, we must solve the immediate issues.

Businesses need funds now for cash flow as that was the aim of the scheme yet bureaucratic application processes, the time taken to process them, hotlines being too busy to process calls and some lenders under the British Business Bank refusing to lend have merely exacerbated the issues.

The current state of affairs is simply not good enough. There is also a need for Government oversight here whereby rates for various lending thresholds should be mandated at capped rates of interest.

Sadly, it would appear that the reduced risk of lending has simply not been priced into the products banks are offering under this scheme.

In Conclusion

Most start-ups and SMEs were lacking capabilities to easily raise capital to finance their inceptions or their projects prior to this crisis. Bank loans were either too expensive or not even an option for most SMEs as banks often require assets to back the loans.

The CBILS was intended to provide respite for unforeseen circumstances, however unfortunately, the early signs are that it is not. Urgent action is needed by the Government to ensure that this is addressed before it is too late.

It is time for the banks to step up, even if this has to be ensured through coercion by whatever means the Government can.

Disclaimer: The views and opinions expressed in this article are those of the author and do not necessarily reflect the official policy or position of any agency, organisation, employer, company or of the U.K. Government. Examples of analysis performed within this article are only examples. They should not be utilised in real-world analytic products as they are based only on very limited and dated open source information. Assumptions made within the analysis are not reflective of the position of any agency, organisation, employer, company or U.K. Government entity. The author of this article or any website or publication where it is published are not to be held responsible for misuse, reuse, recycled and cited and/or uncited copies of content within this article by others.

Hirander has expertise in extensive electronic trading and FinTech spanning 25 years, with successful syndication to investors and substantial exits. He is the Chairman & CEO of GMEX Group and its climate fintech platform-as-a-service ZERO13, which won the COP 28 UAE TechSprint for the use of blockchain to scale climate finance. He is one of the Top 10 influential business leaders of blockchain technology in the UK All Party Parliamentary Group report. He is also featured in LATTICE80’s Top 100 influencer list for the UN Sustainable Development Goals agenda for pioneering blockchain technology solutions. Hirander was also recognised as the Most Influential CEO 2024 – UK (Carbon Credits) by CEO Monthly, a digital magazine published by AI Global Media.

Previously he was the co-founder and Chief Operating Officer of Chi-X Europe Limited, instrumental in taking the company from concept to successful launch. At the time of his departure in February 2010, Chi-X Europe was the second largest equities trading venue in Europe, just behind the LSE Group, and was subsequently sold to Bats Global Markets (now part of CBOE Global Markets) for $365M.