Over the years, hedge funds have tended to capture the public imagination at times of economic extremes. In boom times, they have been held up to be miracle money-making machines, but in times of economic crisis, they have come in harsh scrutiny from the press, from government regulators, and from the public. The truth is somewhere in between, and at the time of writing, that’s about where we are at with regard to their widespread perception and the wider economic situation, which is neither as desperate as it seemed in 2008 or as buoyant as it was in the years preceding the credit crisis.

Hedge funds can have a positive impact in terms of generating wealth, providing liquidity for the markets, and greasing the wheels of capitalism, but they can also have a negative impact when the culture of greed that drives the whole process goes into overdrive and neglects wider societal responsibilities in favour of profits. Here, we shall tell the story of hedge funds, from their conceptual birth in the boom years of the 1920s through their emergence in the post-war years into their current status as the pre-eminent high-end investment vehicle. It’s a chequered history, to be sure, but it’s nonetheless one that sheds light on the evolution of the cult of wealth throughout the 20th and early 21st centuries.

Birth of the Hedge Fund

The boom years of the 1920s brought about, and were to a large extent driven by, the emergence of the pooled fund as a mainstream method of preserving wealth and providing capital growth for investors. Although pooled funds had been around for over a century beforehand, the spectacular wealth-generating properties of the markets after the Great War created an unprecedented demand for more accessible routes into this money machine. During this decade, a whole host of new investment vehicles came into play, and among them was the Graham-Newman Partnership, which has since been cited by uber-investor Warren Buffet as being the earliest example of a hedge fund.

The investment craze of the 1920s saw millions of dollars poured into the markets, creating what we now refer to as a bubble, and when the overheated capital markets went into a tailspin in 1929, the results were catastrophic. What followed was the Great Depression, and for a time, faith in the markets all but dissipated among a disillusioned and heavily-impoverished public. The vast majority of funds and investment banks shut down under the weight of heavy losses, but a few remained, and many of those that did grew to be powerhouses in the years following the Second World War.

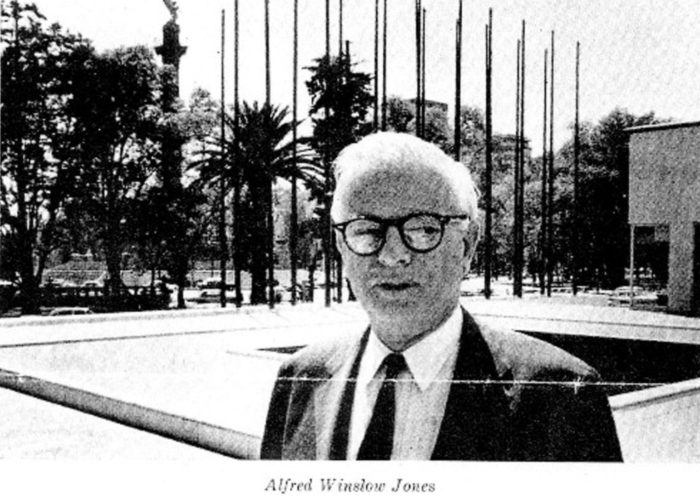

Alfred Jones Hedge Fund Pioneer

Although the strategy of hedging had been explored by investors during the 1920s, it wasn’t until the late 1940s that it became systematized into an investment product. Alfred Jones, considered by many to be the father of the modern hedge fund, was born in 1901 in Melbourne, Australia to American parents. His family moved back to the U.S. while Jones was still a young child, and he later went on to graduate from Harvard in 1923 before going on to serve as a diplomat in Berlin, Germany. He then earned himself a sociology PhD at Columbia University before joining the editorial staff at Fortune magazine in the early 1940s.

The big turning point in Alfred Jones’ life occurred in 1948 when he was asked by his employers at Fortune magazine to write an article about current investment trends. This inspired him to try his hand at being a money manager in his own right, and with $40,000 of his own money and a further $60,000 solicited from investors, he launched a fund based on the concept of the long/short equities model, which he dubbed the ‘hedged fund”. In addition to this investment principle, he used leverage – the idea of borrowing money at a lower interest rate than the anticipated rate of return from his investment strategy – to enhance the returns from the fund.

In 1952, he changed the structure of his investment vehicle from a general partnership to a limited partnership, and gave the managing partner a 20% cut of the profits from the fund as an added incentive. This made Jones the first money manager to combine the use of leverage, short selling, shared risk through a partnership with other investors, as well as a means of compensation based on investment performance. To a large extent, this investment model remains the template for hedge funds, and this is why Jones is so often credited as being the true hedge fund pioneer.

The Rise of the Hedge Fund

As is so often the case, it took time for the world to catch up with a truly innovative concept, and it was more than a decade before Alfred Jones’ hedge(d) fund idea took off as a major investment vehicle. Again, Fortune magazine holds a place in the story.

In 1966, it published an article that shone a spotlight on an obscure investment that has somehow managed to outperform every mutual fund on the market by double-digit figures over the past year. The investment had also outperformed the mutuals by high double-digits over the last five years. Money managers and investors sat up and took notice, and for the first time hedge funds became a real industry. Just two years later, there were 140 hedge funds in operation.

During the boom years of the 1960s, the hedge fund industry underwent a period of frantic expansion, but the recession of 196970 and the 19731974 stock market crash put the kibosh on this growing trend, in the same way that previous and subsequent recessions had done to the investment industry in general. It didnt help that by this time many funds had turned their back on Jones original strategy by engaging in much riskier strategies based on long-term leverage. As a result, many fund suffered heavy losses during the bear markets of 1969-70 and 1973-74.

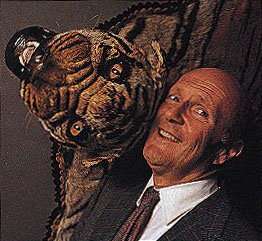

Having had their fingers burned badly by the market downturns of the late ’60s/early ’70s, hedge funds found themselves very much out of fashion among investors. However, in an echo of the original hedge fund boom, the tide turned in 1986 when an article in Institutional Investor shone the spotlight on the phenomenal double-digit success of Julian Robertson’s Tiger Fund.

In 1980, Julian Robertson started the Tiger fund with $8 million in start-up capital. By the late ’90s – the peak of this fund’s performance – the fund was worth over $22 bilion, and in 1993 Robertson was estimated to have made $300 million personally from the fund. Although his actual methods were a lot more subtle than his public pronouncements might have indicated, Robertson expressed the basic philosophy behind the fund as follows:

“our mandate is to find the 200 best companies in the world and invest in them, and find the 200 worst companies in the world and go short on them. If the 200 best don’t do better than the 200 worst, you should probably be in another business.”

The performance of this high-flying hedge fund inspired a flood of interest among investors in the world of hedge funds, and by this point the industry had evolved substantially. In their new incarnation, hedge funds employed a much bigger variety of strategies including derivatives and currency trading.

The Bubble Bursts Once Again

The bull market days of the early 1990s saw a huge outflow of top market talent from the mutual fund industry into the hedge fund industry, where they enjoyed far greater flexibility and renumeration. The high-profile success of George Soros and Jim Rogers’ Quantum Fund – particularly the trade that forced the exit of the UK from the European Exchange Rate Mechanism – only fanned the flames.

But just as hedge funds suffered hugely during the 70s market crash, a similar fate would befall many hedge funds when the dot-com bubble burst in the late 1990s and early 2000s.

Several high-profile funds failed in spectacular fashion, including Long Term Capital Management in 1998, the collapse of Robertsons own Tiger Fund in March 2000, and the enforced reorganisation of George Soros’ and Jim Rogers’ Quantum Fund into the Quantum Group of Funds just one month later.

The Modern Hedge Fund

Following the dot-com crash of 2000 and the global economic crisis of 2008, regulators have clamped down on the previously regulation-light world of hedge funds.

For instance, the U.S. Securities and Exchange Commission (SEC) implemented changes that require hedge fund managers and sponsors to register as investment advisors in 2004. As a result, the number of requirements placed on hedge funds has increased greatly, such as hiring compliance officers, creating a code of ethics, and being sure to keep up-to-date performance records. Essentially this was all done with the intention of protecting investors.

Today, despite recent troubles, the hedge fund industry continues to flourish once more. Crucial to its success was the development of the fund of funds, essentially a hedge fund with a diversified portfolio of numerous underlying single-manager hedge funds.

The introduction of the fund of funds allowed for greater diversification, thereby taking some of the risk out of hedge funding, but also allowed minimum investment requirements of as low as $25,000. This greatly opened up the hedge fund investment option to a far greater number of average investors than ever before.

Hedge Funds Today

Todays hedge funds look significantly different to their forerunners of the 1940s, and even the 1980s. A far greater variety of strategies is used by todays hedge funds, including many that do not involve traditional hedging techniques at all.

The size of the industry is now absolutely vast. While Albert Jones started the first hedge fund with just $100,000,in 2013 the global hedge fund industry recorded a record high of US$2.4 trillion in assets under management.

I am a writer based in London, specialising in finance, trading, investment, and forex. Aside from the articles and content I write for IntelligentHQ, I also write for euroinvestor.com, and I have also written educational trading and investment guides for various websites including tradingquarter.com. Before specialising in finance, I worked as a writer for various digital marketing firms, specialising in online SEO-friendly content. I grew up in Aberdeen, Scotland, and I have an MA in English Literature from the University of Glasgow and I am a lead musician in a band. You can find me on twitter @pmilne100.

{kind=link}